Multinational Investment Bank + Financial Services Firm

Personal Loans (PL) are effective tools for paying down and eliminating debt.

Our client, a multinational financial services firm, was puzzled as to why 50% of

their customers failed to consolidate their debt after taking out a loan for that very reason.

Even though 80% of customers indicated consolidation as the reason for their loan, only 40%

of customer debt ($) was being consolidated — some being spent on other uses.

What ensued was a 12-week exploration of the customer experience that culminated in the

development of strategies and prototypes to support customers’ debt consolidation goals.

Defining the Problem

Beyond Data:

Because data was only telling half the story, we spoke with 82 customers to empathize with the application process and loan usage behaviors. I soon realized a stark contrast between how customers and our client thought about personal loans.

Disconnect:

Business Lens: Client felt that customers were being economically irrational.

Behavioral Lens: Something was getting lost in translation in addition to contextual and emotional factors at play.

“My kid broke his arm and I took out a loan because after the hospital bills I needed cash quickly. I knew exactly what the loan’s purpose was, but then I had a school loan that I was playing catch up with…”

— Research Participant

Pictured above is an example of one of the 12 situations that our research participants experienced in the game. We explored situations before, during, and after the loan was disbursed. In this example, participants use a tablet to select one of the three multiple choices option on the screen.

Game-Based Simulations

Testing interventions:

I developed an immersive game-based simulation and learned exactly why customers and our client have such different understandings. Game-based research like this is helpful in getting inside the heads of our clients’ customers.

Game Play

Groups of 10 participants are shown 12 different situations. A situation includes: (i) context (ii) a question about a decision, and (iii) three multiple-choice options. Points are awarded if the option chosen is also the response chosen by the majority.

Debt as a Feeling

User Insights

As debt accumulates, participants coped by revising their debt threshold. Only after a financial shock will someone feel like they are in debt. Customers become hyper-focused on short-term payment management, not wholistic debt elimination. When customers feel confident they are more likely to consolidate as intended, and less likely to feel like they are in debt.

Pictured above is an alternative user flow that allows customers to more fully and clearly articulate their intention for the loan. By clarifying the intent the user feels more confident in how their loan is planned to be used.

Phase 1: Design for Confidence

Reframing the Problem:

My strategy was to design for confidence, Those who are confident are more likely to consolidate debt as intended. Customers feel confident by (i) clarifying intent/s and (ii) planning loan amount accordingly

Solution:

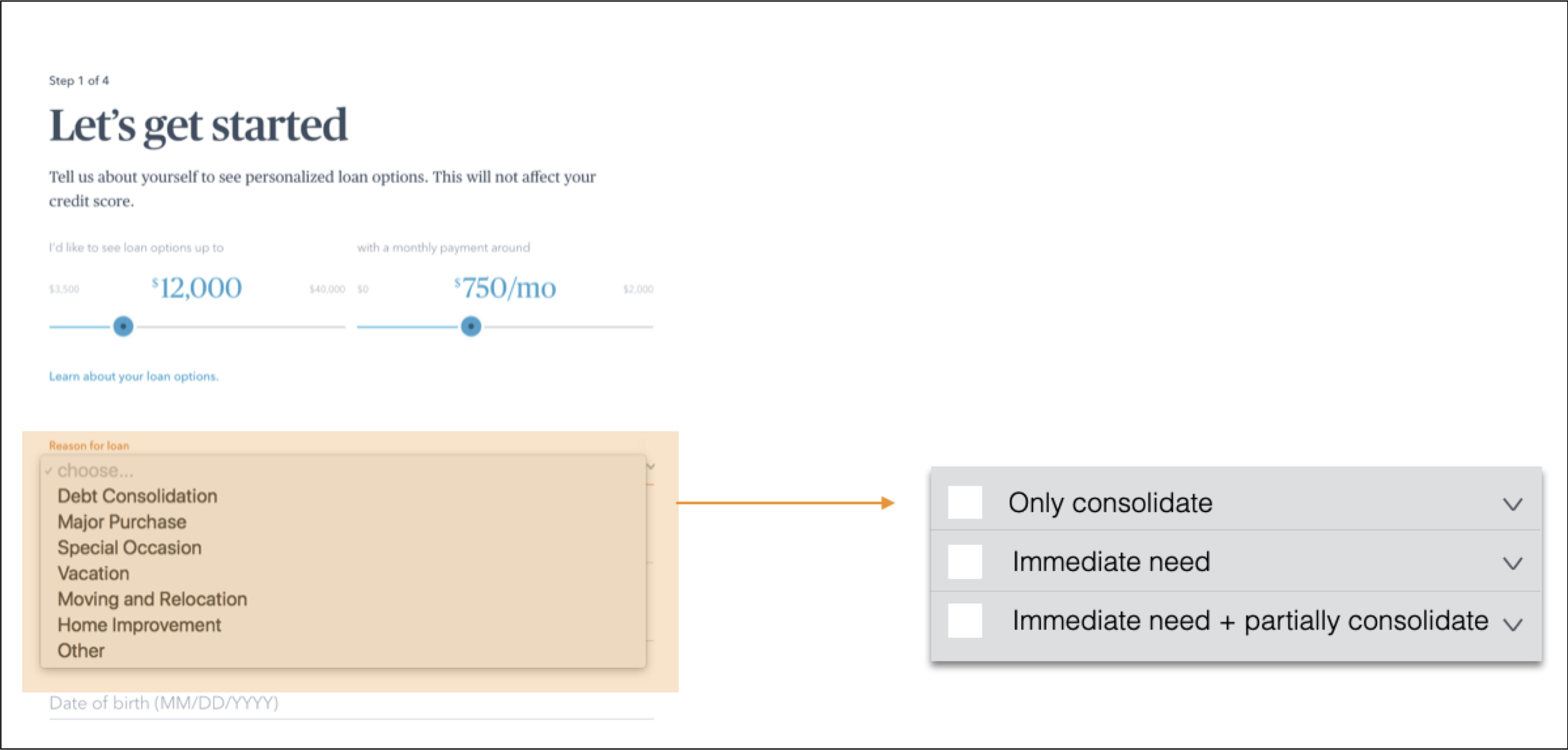

My first recommendation was to include a drop-down menu option to anticipate multiple intents + different levels of consolidation. Currently the user flow doesn’t allow for customers to express more than one intent.

Pictured above is a re-imagined user flow in which customers must first select their reason(s) for the loan. By clarifying their intention, users feel more confident in the loan amount calculation and their ability to consolidate debt.

Phase 2: New User Roadmap

Current User Flow:

When customers begin their application they must immediately declare their desired loan amount. Only after a loan amount is selected are users asked how the loan will be used.

Revised User Flow:

We recommended switching the order of the reason for loan and loan amount fields. Customers must first clarify their intention for the loan. This will help users confidently arrive at an optimal amount.

Pictured above is a Loan Planning tool that is designed to legitimize the kinds of uses that a customer may have for their loan, and to help customers feel more confident in their desired loan amount.

Phase 3: Loan Planning Tool

Behavioral Principles:

(1) Anchoring on the right number:

Introduce users to three common loan uses: immediate need; consolidation; and, security

Allow them to see and build their loan amounts organically

Anchor to a more realistic amount, not a guess

(2) Choice architecture

Choice architecture changes the way decisions are considered and made based on how information is categorized

Percentages and absolute numbers are used independently to align with how users frame these categories.

Achieve optimal loan amounts.